53% of Americans Now Prefer Buying Over Renting. Here's What That Means for You

Bank of America's 2026 survey shows 53% of Americans now prefer buying over renting. Here's what it means for you.

For the first time since 2023, more Americans say buying beats renting.

That’s the headline stat from Bank of America’s 2026 Homebuyer Insights report. Based on responses to their national online survey, 53% of respondents say it’s better to buy a home in the current market than to rent or move in with family (47%).

Aside from that, other stats from the survey reveal some interesting trends, including improved levels of optimism around buying a home, despite ongoing affordability challenges.

Read on to see why and how this impacts you as a buyer or seller in [Your Market].

How Americans Feel About Homeownership Right Now

According to the methodology details for Bank of America’s 2026 survey, respondents are adults 18 years of age or older who “make or share in household financial decisions, and who currently own a home/previously owned a home or plan to own a home in the future.”

Of the 2,000 respondents in BofA’s survey:

1,000 are homeowners

1,000 are renters who have either owned homes previously or plan to own a home

The resulting data is compared to last year’s survey results, showing an overall improvement in consumer sentiment on homeownership and homebuying conditions:

90% say a home is a valuable investment (up from 79%);

94% say it provides stability (up from 83%);

87% say it feels like a milestone (up from 78%);

86% say it brings emotional fulfillment (up from 75%)

Beyond the abstract numbers, the data provides a signal of where consumer sentiment is heading, at least on a national level. But without the breakdown by respondent type (owners and renters separately), it’s unclear what percentage of renters are feeling better about their homebuying prospects this year compared to last.

Fewer Buyers Are Waiting for the Perfect Moment

Plenty of homebuyers in 2026 are still holding out for lower home prices and lower mortgage rates, but that share has dropped from 75% in 2025 to 71% in 2026.

Gen Z and Millennial buyers are especially motivated to buy, driving this year’s shift toward action:

Gen Z (68% are holding out in 2026 vs. 74% in 2025)

Millennial (70% holding out in 2026 vs. 77% in 2025)

As for Gen Z, survey data highlighted three specific ways they’re adapting to today’s market:

28% are taking on extra jobs

32% are considering co-buying with friends or family

31% are planning to leverage down payment assistance programs

Data comparing 2026 to the previous couple years is also showing an increased willingness to move across all three well-known compromise scenarios:

A more affordable area: 76% in 2026 vs. 71% in 2025 and 68% in 2024

Their dream home becoming available: 75% in 2026 vs. 69% in 2025 and 67% in 2024

A better location: 71% in 2026 vs. 65% in 2025 and 63% in 2024

Also, 52% of the homeowners in BofA’s survey say they expect to buy again, while 22% plan to move within the next year (up from 15% in 2025).

Why Affordability Is Still the Biggest Hurdle

Bank of America’s data for 2026 showed a year-over-year increase in survey respondents citing affordability constraints as an obstacle to homeownership:

58% cited expensive home prices as a top barrier, up from 46% in 2025

47% cited high interest rates, up from 40% in 2025

Based on their responses, renters are also trading down to cut housing costs.

For some, that means moving to a more affordable rental complex. For others, it could mean moving to a unit with fewer bedrooms. In some markets, a drop from a two-bedroom to a one-bedroom unit can save a renter around $200 a month.

What This Means If You're Thinking About Buying or Selling

The biggest takeaway from Bank of America's survey isn't that the market suddenly became easy. Affordability is still a challenge, and mortgage rates remain higher than many buyers would like.

What's changing is consumer mindset.

After several years of waiting for the "perfect" time to buy, more Americans appear to be accepting that today's market may simply be the market they'll have to navigate. Instead of waiting indefinitely, many are adjusting their expectations, exploring different neighborhoods, considering smaller homes, or taking advantage of down payment assistance programs.

That's an important shift because housing markets don't move based only on prices and interest rates. They also move based on confidence. When more buyers decide they can make today's conditions work, activity tends to follow.

National surveys can only tell part of the story, and every local market behaves differently. But they do offer a useful glimpse into how consumers are thinking. Right now, that thinking seems to be moving away from waiting for perfect conditions and toward finding opportunities within the market that exists today.

Stafford & Rebecca | Compass Real Estate Atlanta

Foreclosures Hit Their Highest Level in 6 Years. Here’s What That Means for Buyers

A new Realtor.com report shows foreclosed homes selling 27.2% below value. Here is what that means for home buyers in 2026. Stafford & Rebecca | Compass | Atlanta

In the first half of 2026, buyers saved about 27% on foreclosed homes listed for sale.

And as of April, foreclosure listings made up 1.3% of total for-sale listings, the highest level in six years.

New data from Realtor.com also shows foreclosed property listings, also called REO listings, are getting 26.5% more page views compared to typical home listings.

Yet they still sit 11 days longer, partly because foreclosure has a scary reputation for a lot of homebuyers. But that’s not the only reason.

While these properties could be hidden opportunities, they’re not without risk.

Here’s what’s driving the rise in foreclosures and the trade-offs that go with buying an REO property vs a seller-owned or newly-built home.

By the time you’re done reading this, you’ll know what to expect in [Your Market] and whether these homes are worth looking into.

Why Foreclosures Are Ticking Up Again

Foreclosure listings reached their highest level in April, hitting 1.3%. It’s still shy of the recent high of 1.7% from 2020, and it’s nowhere near the levels seen during the Great Financial Crisis.

The increase in foreclosures has a lot to do with forbearance and moratorium programs from the pandemic era that fully wound down in 2024. Owners who bought at peak prices were then squeezed by rising insurance costs, rising property taxes, and resetting payments for adjustable rate mortgage (ARM) loans.

In short, the cost of keeping their home grew significantly faster than their household income could make up for it.

But as Realtor.com senior economist Joel Berner explained it, that increase is the market normalizing, not a sign of another mortgage crisis.

That said, there are some things you need to know about buying an REO property.

What You Actually Get, and Give Up, With a Foreclosure

First things first: “What’s an REO?”

When a foreclosed property fails to sell at auction, it becomes a “Real Estate Owned” (REO) property, which is when a lender repossesses a home. When it is put on the market as a foreclosure listing, it’s often priced below market value in order to sell as quickly as possible.

Instead, these homes would sit an average of 11 days longer on the market (nationwide).

Here’s why:

REOs have 30.4% fewer photos than standard listings

Descriptions for REO homes are 33% shorter than for standard listings

Many REOs sell as is (the buyer absorbs repairs)

As a buyer, though, you can still get interior inspections. You can still tour the home. You can still work with a real estate agent who can look into the property’s history (flooding, septic issues, bug/rodent/snake infestations, property damage, etc.) and help you avoid an expensive mistake.

Also, to answer another common question, conventional financing is still an option.

So, is this something you should look into?

Should You Consider Buying a Foreclosure?

The answer depends on your priorities.

If you're looking for a move-in-ready home with fewer surprises, a traditional resale or new construction home may be a better fit. Foreclosures often require more patience, more due diligence, and sometimes additional money after closing for repairs and updates.

On the other hand, if you're comfortable taking on a project—or you're simply looking to maximize your budget—a foreclosure could be an opportunity to buy a home for less than comparable properties in the area.

Before making an offer, here are a few things to look for:

Potential advantages

Lower purchase price than similar homes

Less competition in some markets because many buyers overlook foreclosures

Opportunity to build equity through repairs and improvements

Conventional financing may still be available on many REO properties

Potential drawbacks

Homes are typically sold as is, with limited or no seller repairs

Deferred maintenance or hidden issues can increase renovation costs

Utility systems may have been unused for extended periods and need repairs

Limited property information may mean you'll need to do more research

The key is working with an agent who can help you evaluate whether a lower purchase price actually outweighs the cost of repairs and future maintenance. A discounted home isn't necessarily a good deal if it comes with expensive surprises.

-Stafford Weber | Compass Real Estate

Home Insurance Costs Are Up 46% Since 2021. Here's How to Fight Back.

Home insurance costs have climbed 46% since 2021, and 71% of homeowners are feeling it. Here's what homeowners can do right now to lower their premiums. - Stafford and Rebecca | Compass

If your homeowners insurance bill went up this year, you're not alone. According to a recent Pew Research Center survey, 71% of U.S. homeowners say their insurance costs have increased over the past few years. And it's not a small bump for most people. A full 42% say their costs have gone up "a lot."

Here in Atlanta, I've been hearing the same thing from my clients. People open their renewal notice and do a double take. Some are calling their insurer for the first time in years.

The good news is you're not stuck. There are concrete steps you can take to bring your premium down without putting your home at financial risk.

Let’s walk through what's actually driving these increases and what's worth trying right now.

Why Premiums Have Climbed So Fast

The short version: insurance companies have been paying out a lot more in claims, and they're passing that cost on to policyholders.

According to the Consumer Federation of America (CFA), the average annual home insurance premium has climbed 24% since 2021, reaching $3,303 per year. That's twice the rate of inflation over the same period, and the increases have been adding up to real money: the typical homeowner is now paying $648 more per year than they were four years ago.

The main culprits are severe weather and rising rebuilding costs. More frequent storms, wildfires, floods, and hail events mean more claims. And when those claims do get paid, the cost to repair or rebuild a home is significantly higher than it was a few years ago. Labor and materials are more expensive. Insurers are recalibrating.

CFA found premiums increased in 95% of U.S. ZIP codes between 2021 and 2024. No region has been spared.

What's Probably Driving Your Specific Bill

The national average tells you where things are trending, but your individual premium depends on a mix of factors that are specific to you and your home.

The biggest ones insurers look at:

Where your home is located. Proximity to flood zones, wildfire risk areas, or regions with frequent severe storms will push your rate up. Even being in a high-crime ZIP code can affect your premium.

Your home's age and construction. Older homes (especially those with older roofs, wiring, or plumbing) are more expensive to insure. Upgrades to these systems can sometimes lower your rate.

Your claims history. Filing claims, even small ones, can raise your premium at renewal. Insurers also look at the claims history of the property itself, not just you as the owner.

Your credit score. In most states, insurers can factor in credit history when pricing a policy. A strong credit score can work in your favor.

Your coverage limits and deductible. Higher coverage limits mean a higher premium. A lower deductible means the insurer takes on more risk, and charges accordingly.

Understanding which of these factors is driving your bill is a good starting point before you do anything else.

5 Things You Can Do Right Now

You don't have to just absorb the increase. Let’s talk about real steps that are helping people reduce their rates in [Your Market].

1. Shop your policy every single year.

Most people set their homeowners insurance and forget it. That's expensive. Loyalty doesn't get rewarded in this market. Get at least two or three competing quotes at renewal time. Online marketplaces like Insurify or Policygenius make this faster than it used to be. Switching carriers can save hundreds of dollars a year, and you don't have to wait until your renewal date to start looking.

2. Raise your deductible.

If you can comfortably cover a higher out-of-pocket cost in the event of a claim, raising your deductible from $1,000 to $2,500 or even $5,000 can significantly lower your annual premium. Think of it as self-insuring for smaller losses and keeping coverage for the big ones.

3. Bundle your home and auto policies.

Most major insurers offer a discount for bundling home and auto coverage under the same company. If yours are currently with different carriers, it's worth pricing out a bundle. The savings aren't guaranteed to be dramatic, but they add up over time.

4. Ask about mitigation discounts.

Many insurers will lower your premium if you've made your home more resistant to damage. A new roof, storm shutters, updated electrical panel, a whole-home generator, a monitored security system. These can all qualify for discounts depending on your insurer and your location. Call and ask specifically. These discounts aren't always advertised.

5. Review your coverage limits.

If your home's market value has shifted significantly, your coverage limits may be out of sync with what you actually need. You don't want to be underinsured in a major loss, but you also don't want to be paying to insure a higher rebuild cost than your home actually requires. A quick conversation with your insurer about your dwelling coverage amount is worth having.

A Note on Dropping Coverage

When the bill goes up, the temptation to drop or gut your policy is real. According to CNBC, more than one in four homeowners say they'd drop their coverage if they could. That's an understandable reaction. It's also one of the riskiest moves a homeowner can make.

That's an understandable reaction, but it's one of the riskiest moves a homeowner can make.

A single storm, fire, or burst pipe can cost tens of thousands of dollars out of pocket. If you have a mortgage, your lender almost certainly requires you to maintain coverage. If you let it lapse, they'll place what's called "force-placed insurance" on the property, which is typically far more expensive and far less comprehensive than a policy you'd choose yourself.

If the cost is genuinely unmanageable, the better path is to raise your deductible, reduce optional coverage riders, or shop aggressively for a better rate.

Dropping coverage entirely or cutting limits so low they don't reflect your actual risk only defers a much bigger potential cost.

You Have More Leverage Than You Think

The insurance market is frustrating right now. Premiums are up, options in some areas are narrowing, and renewal notices don't come with a lot of explanation.

Pick one thing from this list and act on it before your next renewal. Even shopping your rate once a year puts you in a much stronger position than most homeowners.

You may not be able to undo the national trend, but you can make sure you're not paying more than you have to for the coverage you need.

-Stafford Weber | Compass

The Real Estate Red Flag Guide Every Atlanta Buyer Needs Before Making an Offer

A guide for Atlanta buyers on which home inspection red flags to walk away from, negotiate on, or get a second opinion about before closing.

Buying a home is exciting. It can also make you do things you'd never do with any other purchase, like convince yourself that a little mold in the basement "probably isn't a big deal."

You're not alone. According to a 2026 survey by Clever Real Estate, 76% of home buyers would be willing to overlook red flags in a home. And in some cases, it really isn’t a big deal. Not every red flag means you should run.

The key is knowing which problems are negotiating leverage, which ones need a closer look, and which ones should send you straight back to the car.

Here's how I break it down for my buyers.

Which red flags are actually opportunities?

Some things that scare off other buyers can actually work in your favor. If you spot one of these, don't panic, strategize.

A home that's been sitting on the market.

Almost half of buyers (43%) say a long time on market makes them suspicious. But a home that's been listed for 60+ days in Atlanta usually means one thing: a motivated seller.

That's your opening to negotiate on price, closing costs, or repairs. Ask me why it's been sitting; the answer is usually fixable.

A home that fell out of contract.

Only 20% of buyers flag this as concerning, and they're right not to overreact. Deals fall apart for dozens of reasons that have nothing to do with the house. The buyer's financing fell through, they got cold feet, or they couldn't sell their current home.

Cosmetic issues.

Ugly paint, dated fixtures, overgrown landscaping, worn carpet. These scare away buyers who can't see past the surface.

If you can, you'll face less competition and often get a better price.

A $5,000 cosmetic refresh on a home you bought for $15,000 under asking? That's a win.

A prior foreclosure.

Only 24% of buyers see this as a red flag.

By the time a foreclosed home hits the FMLS, the title is typically clean and the bank just wants it sold. These can be some of the best deals in Atlanta if you do your due diligence.

Which red flags need a professional opinion before you decide?

These are the ones where the cost can range from "totally manageable" to "walk away." The difference is almost always in the details, which is why you never skip the inspection.

Mold or water damage.

Here's a stat that surprised me: 49% of buyers say mold isn't a dealbreaker. That's fine, as long as you know the math.

A small patch of bathroom mold might cost $500 to $1,500 to remediate. Mold throughout a crawlspace or behind walls? That's $10,000 to $30,000.

The mold itself isn't the dealbreaker. The scope is. Always get a mold specialist's estimate before you decide.

Foundation or structural problems.

Nearly half of buyers surveyed (45%) would still purchase a home with major structural issues. I get it. In Atlanta’s market, you don't want to lose a home you love.

But the range here is massive: a minor crack might cost $250 to $800 to seal with epoxy. Foundation piering or major stabilization can run $10,000 to $23,000.

Get a structural engineer's assessment. It costs a few hundred dollars and could save you tens of thousands.

Signs of pests.

A full 57% of buyers say pests aren't a dealbreaker, and in many cases, they're right. A standard pest treatment runs a few hundred bucks.

But termite damage is a different story. Repairs for termite damage average $3,000 to $8,000 and can exceed $15,000 if structural elements are compromised.

The treatment is cheap. The repair bill is where it gets expensive.

Electrical problems.

More than half of buyers (54%) would proceed with electrical issues. Minor fixes are routine. But if the home needs a full rewire, you're looking at $8,000 to $15,000.

Have your inspector flag the panel and wiring type. Knob-and-tube or aluminum wiring is a bigger conversation, because some insurance companies won't cover it.

Plumbing or water pressure issues.

Another 57% of buyers aren't deterred by plumbing problems. Low water pressure might just need a new pressure regulator ($200 to $400). But if you're dealing with corroded pipes, a failing sewer line, or galvanized steel plumbing, a full repipe could cost $4,000 to $15,000.

Which red flags should make you walk away?

These are the ones where no amount of negotiation fixes the problem. The house might be perfect in every other way, but these issues either can't be resolved or will cost you indefinitely.

Environmental contamination nearby.

The Clever survey found that 59% of buyers would overlook nearby environmental contamination.

That's concerning. You can renovate a kitchen. You can't move a Superfund site, a leaking underground storage tank, or industrial runoff.

Check the EPA's Envirofacts database and Atlanta’s environmental records before you fall in love with a property near industrial or commercial zones.

Flood zone without affordable insurance.

More than half of buyers (56%) say a flood zone isn't a dealbreaker. But flood insurance costs have been rising sharply under FEMA's Risk Rating 2.0, and in some areas, annual premiums can exceed $3,000 to $5,000 on top of your regular homeowners policy.

Before you make an offer on any property near water or in a low-lying area, check FEMA's flood maps and get an insurance quote. If the numbers don't work, neither does the house.

Unresolvable title issues.

Liens from unpaid contractors, boundary disputes with neighbors, unresolved estate claims, undisclosed easements can all delay or kill a closing and haunt you for years after.

Title insurance covers a lot, but it doesn't cover everything. If the title search turns up complications that can't be cleared before closing, it's usually not worth the risk.

A note for first-time buyers

If you're in your 20s or early 30s buying your first home, this part is for you.

The Clever survey found that younger buyers are significantly more willing to take on serious defects to get into the market. 62% of Gen Z buyers would purchase a home with mold (compared to 40% of boomers). 61% would buy with hazardous materials. And more Gen Z buyers said bad cell phone service is a bigger dealbreaker than cracks in the ceiling.

I understand the urgency. Atlanta’s market isn't easy for first-time buyers, and the pressure to stop renting and start building equity is real. But the most expensive home is the one that costs you $30,000 in repairs six months after closing.

You don't have to buy a perfect home. You just need to know exactly what you're buying and what it'll cost to fix. That's what I'm here for.

The bottom line

Red flags aren't all created equal. Some are opportunities in disguise. Some need expert evaluation before you decide. And some should send you looking at the next listing.

The trick is having someone in your corner who knows the difference and who'll be honest with you even when it means slowing things down.

-Stafford Weber | Compass

43% of Homeowners Are Equity Rich. Are You One of Them?

New data shows nearly half of all mortgaged homes in the U.S. are equity rich. If you own a home in Atlanta here's what that means for your options.

If you own a home in Metro Atlanta, there's a good chance you're sitting on more equity than you realize.

New data shows 43.3% of mortgaged homes across the country are equity-rich right now.

At the same time, a separate survey from Point found that 48% of homeowners say they aren't planning to move this year, but not for the reasons you may think.

A lot of them assume they're stuck, mostly because of where mortgage rates are sitting. But being equity-rich changes the calculation in ways most people haven't thought through yet.

So, today, I’m breaking down what the data actually shows, why so many homeowners feel locked in place, and what your equity could actually mean for your options.

What Does "Equity Rich" Actually Mean?

"Equity-rich" is a specific term used in real estate. It means you owe less than 50% of what your home is currently worth.

So if your home is worth $400,000 and your remaining mortgage balance is $180,000, you're equity-rich. You have more than half the home's value sitting on your side of the ledger.

Equity-rich means you don't just have equity in your home. It means you have a lot of it, enough to give you real financial options you may not have considered.

What the Numbers Show

Why So Many Homeowners Feel Stuck

If you locked in a mortgage rate at 3% a few years ago, the idea of selling and buying again probably doesn't sound appealing.

With 30-year rates currently sitting at 6.42% and no Fed cuts expected until late 2027, trading your current payment for one that's nearly double is a hard sell. No one would blame you for hesitating.

After all, a recent survey from Point found 48% of homeowners (nearly half) say they aren't planning to move this year, with rate lock-in and general uncertainty cited as the main reasons.

What that rate calculation doesn't account for, though, is how much equity you have, and how much that could save you each month on your next mortgage payment.

How Your Equity Changes the Math

When you're equity-rich, you're not approaching your next purchase the same way you did the first time.

A larger equity position means a larger down payment, which means a smaller loan, which means your monthly payment on a higher-rate mortgage may not be as painful as you'd expect.

Depending on how much equity you've built, you may have more options than you think:

Put a significantly larger down payment on your next home, reducing the loan amount and softening the rate impact

Use a HELOC to access equity without selling

Sell, then rent temporarily while you wait for rates or prices to shift

Buy your next home outright, with no mortgage at all

Most homeowners run the math on today's rates without accounting for what their equity actually does to that number. The monthly payment picture looks very different when you're bringing 50% or more to the table.

What This Could Mean for You

The bigger takeaway here is this: A lot of homeowners are making decisions based on the market from 2-3 years ago, not the market we’re actually in today.

Yes, rates are higher.

But home values are also dramatically different, and for many homeowners, the amount of equity they’ve built changes the conversation more than they realize.

You may still decide staying put is the right move. A lot of people are. But it’s worth understanding your position before assuming you don’t have options.

Because the homeowners making the best decisions right now aren’t guessing. They know their numbers. ATTOM’s Q1 2026 report shows 43.3% of mortgaged U.S. homes are equity-rich, meaning owners owe no more than half of what their home is worth. Georgia is slightly below the national figure at 41.9%, down from 44.0% last quarter and 43.7% a year ago. Atlanta’s market is also shifting: April 2026 data showed pending sales down year over year, while median sales price rose to $417,000, which points to a more selective market rather than a collapsed one.

Atlanta homeowners are still sitting on real equity.

ATTOM’s Q1 2026 report shows that 41.9% of mortgaged homes in Georgia are considered “equity rich,” meaning the owner owes less than half of what the home is worth.

Nationally, that number is 43.3% — the lowest level since late 2021, but still a powerful reminder of how much wealth homeowners have built over the last several years.

Here’s why that matters in Atlanta:

Many sellers have options.

Many buyers are waiting for the right home.

And the homes that are well-prepared, well-priced, and well-positioned are still the ones creating movement.

This is not the 2021 market. It is also not a market to sit out if your move would improve your life.

Equity gives sellers leverage. More inventory gives buyers opportunity. And strategy matters more than ever on both sides.

If you’re wondering what your home is really worth in today’s Atlanta market — or how much equity you may have to work with — message me. This is exactly the kind of conversation worth having before you make your next move.

What’s the Best Week to List Your Home in Atlanta? Here’s What the Data Says

When is the best time to sell your home in Atlanta in 2026? Here’s what the data reveals, and how to choose the best time for you. -Stafford Weber | Compass

We get asked all the time “when is the best time to sell my home?”

Right now, the data gives two answers within a 5-week timeframe of each other. Realtor.com says mid-April. Zillow says late May.

That doesn’t mean one is right and the other is wrong. It means there’s more than one way to approach your timing depending on what matters most to you.

Let’s take a look at what each one means for you as a seller in Atlanta

The Mid-April Window: Why Listing Earlier Can Work in Your Favor

Realtor.com points to mid-April as a strong window to list your home for sale because buyers are already active, and the number of homes for sale hasn’t peaked yet.

In many markets, this is when serious buyers start making moves. They’ve been watching listings for weeks. They’re ready to act when something new hits the market.

Here’s why this window can work in your favor:

Fewer competing listings than in May and June, which can help your home stand out

Buyers who are ready to write offers, not just browse

More attention on each new listing as fresh inventory hits the market

A chance to get ahead of the late spring surge of new sellers

What this looks like in Atlanta can vary. In some areas, buyer activity picks up earlier. In others, it builds closer to late spring. The key is understanding when buyers in your area start paying attention and being ready when they do.

If you list during this window, you’re stepping into the market when demand is building, and competition is still manageable. That can put you in a strong position as a seller.

The Late May Window: Why Waiting Can Push Your Price Higher

Zillow points to a later window, the last two weeks of May, as a strong time to list if your goal is to maximize your sale price.

By this point in the spring, buyer activity is at its highest. More people are actively searching, scheduling showings, and preparing to make offers. Many are working around summer plans or school timelines, which adds a sense of urgency.

Here’s why this timing can work in your favor:

A larger pool of buyers actively looking

More competition among buyers, which can lead to stronger offers

Higher sale prices during peak demand periods

Increased chance of multiple offers on well-priced homes

In Atlanta, this often shows up as busier open houses, more showings in a shorter window, and buyers moving faster when they find the right home.

Waiting until this window can create the kind of competition that pushes your final sale price higher. The trade-off is that more sellers are also entering the market around the same time, which means your home needs to be positioned well from day one.

What Matters More Than the “Perfect Week”

It’s easy to get caught up in finding the exact right week to list. In reality, your outcome depends more on what’s happening in Atlanta right now.

Every market has its own rhythm. Some neighborhoods heat up earlier in the spring. Others take a little longer to build. Price point and property type also play a role in how quickly buyers respond.

Here are a few things that matter when deciding when to list:

How many homes are currently for sale in Atlanta

How quickly homes are going under contract

Whether buyers are competing or taking their time

How similar homes to yours are being priced and received

This is where local insight comes in. Looking at national trends can give you a starting point, but the real value comes from understanding how those trends show up in your area.

When you combine timing with the right pricing, presentation, and marketing plan, you put yourself in a much stronger position as a seller.

What This Means for You as a Seller

If you’re thinking about selling this spring, your timing should line up with your goals and what’s happening in Atlanta.

Some sellers choose to list earlier, when there are fewer homes to compete with and buyers are already watching for new inventory. Others wait for a busier stretch, when more buyers are active and ready to make offers.

Your situation will guide that decision:

How quickly you want to sell

How important price is in your decision

What your home offers compared to others in Atlanta

Having a clear plan before you list will put you in a stronger position.

That starts with understanding your local timing and preparing your home for the market.

-Stafford Weber

Team Stafford & Rebecca | Compass | Atlanta

The 5 Greenest Places to Visit in Greater Atlanta (A Local's Guide)

Discover the greenest parks, gardens, and nature preserves in the greater Atlanta area. From the Atlanta Botanical Garden to hidden gems in Roswell and Dunwoody — a local real estate expert's guide to Atlanta's best green spaces.

Atlanta is known as the "City in a Forest" — and for good reason. With one of the highest urban tree canopy coverages in the country, the greater Atlanta area is home to world-class botanical gardens, sprawling urban parks, and peaceful nature preserves that make this one of the most livable metros in the Southeast.

As a local real estate team rooted in the Atlanta area, we spend our days in the neighborhoods surrounding these green spaces — and we can tell you firsthand that access to nature is one of the top reasons people choose to call this city home. Whether you already live here or you're thinking about making the move, here are five of the greenest places in greater Atlanta that are worth knowing about.

1. Atlanta Botanical Garden — Midtown Atlanta

What It Is: The Atlanta Botanical Garden is a 30-acre living landmark in the heart of Midtown, nestled between Piedmont Park and the city skyline. It's home to one of the largest orchid collections in the U.S., a stunning Canopy Walk suspended among the treetops, and seasonal displays — including its famous holiday light installation — that draw hundreds of thousands of visitors each year.

Why It's One of Atlanta's Greenest Places: Few places in Atlanta blend nature and urban life as seamlessly as the Botanical Garden. The Storza Woods section alone is one of the last remaining patches of mature hardwood forest in Midtown, and the garden's conservation programs help protect endangered plant species from around the world. If you live in Midtown, Morningside, or Virginia-Highland, this is practically your backyard.

📍 Location: 1345 Piedmont Ave NE, Atlanta, GA 30309 🌐 Website: atlantabg.org

2. Piedmont Park — Midtown Atlanta

What It Is: Piedmont Park is Atlanta's signature urban park — over 200 acres of open green space right in the center of the city. With wide lawns, wooded trails, Lake Clara Meer, and sweeping skyline views, it's the gathering place for everything from weekend farmers markets to major festivals like Music Midtown and the Atlanta Dogwood Festival.

Why It's One of Atlanta's Greenest Places: Piedmont Park is often called the "Central Park of the South," and it earns that comparison. It's the green heart of Midtown and one of the key reasons neighborhoods like Midtown, Ansley Park, and Virginia-Highland are consistently among the most desirable places to live in Atlanta. Whether you're running the trails, picnicking with your family, or just watching the sunset over the skyline, this park defines the Atlanta outdoor lifestyle.

📍 Location: 400 Park Dr NE, Atlanta, GA 30306 🌐 Website: piedmontpark.org

3. Chattahoochee Nature Center — Roswell

What It Is: The Chattahoochee Nature Center is a 127-acre nature preserve in Roswell situated along the banks of the Chattahoochee River. It features boardwalk trails through wetlands and forest, native wildlife exhibits, river access, and environmental education programs that have served the community for over 45 years.

Why It's One of Atlanta's Greenest Places: This is one of the most immersive nature experiences you can have without leaving metro Atlanta. The preserve protects a stretch of river and forest habitat that feels genuinely wild, yet it's just minutes from the shops and restaurants of downtown Roswell and Canton Street. For families and nature lovers looking at homes in Roswell, East Cobb, or Alpharetta, the Chattahoochee Nature Center is one of the area's biggest lifestyle perks.

📍 Location: 9135 Willeo Rd, Roswell, GA 30075 🌐 Website: chattnaturecenter.org

4. Gibbs Gardens — Ball Ground

What It Is: Gibbs Gardens is a 300-acre estate garden in Ball Ground, about an hour north of Atlanta. It's one of the largest residential-style gardens in the nation, featuring 20 million daffodils in spring, a world-class Japanese garden, and year-round designed landscapes that change dramatically with the seasons.

Why It's One of Atlanta's Greenest Places: Gibbs Gardens offers the kind of grand, immersive garden experience that most people associate with destinations like Longwood Gardens in Pennsylvania or the Portland Japanese Garden. The fact that it's right here in North Georgia — easily accessible from Cherokee County, Woodstock, and Canton — makes it a true hidden gem of the greater Atlanta area. It's a must-visit for anyone who appreciates natural beauty on a grand scale.

📍 Location: 1987 Gibbs Dr, Ball Ground, GA 30107 🌐 Website: gibbsgardens.com

5. Dunwoody Nature Center — Dunwoody

What It Is: The Dunwoody Nature Center is a 22-acre wooded preserve tucked into the heart of Dunwoody. It offers walking trails through hardwood forest, a creek habitat, a community garden, and nature-based programming for kids and families — all within a quiet, residential setting.

Why It's One of Atlanta's Greenest Places: What makes the Dunwoody Nature Center special is its role as a true neighborhood green space. It's not a tourist destination — it's a place where local families walk, learn, and connect with nature steps from their front door. That kind of integrated, everyday access to green space is part of what makes Dunwoody one of the most livable communities inside the perimeter. If you're exploring homes in Dunwoody, Sandy Springs, or Brookhaven, spaces like this are a big part of the quality of life.

📍 Location: 5343 Roberts Dr, Dunwoody, GA 30338 🌐 Website: dunwoodynature.org

Why Green Spaces Matter When Choosing Where to Live in Atlanta

If you're searching for a home in the greater Atlanta area, proximity to parks, gardens, and nature preserves isn't just a nice bonus — it's a lifestyle advantage. Studies consistently show that access to green space improves quality of life, supports property values, and contributes to stronger community connections.

At SR Homes Atlanta, we know these neighborhoods inside and out. We've helped buyers and sellers across Midtown, Roswell, Dunwoody, and beyond find homes in the communities that fit their lifestyle — green spaces and all.

Thinking about making one of these neighborhoods home? We'd love to help you explore your options. Contact us at SR Homes Atlanta to start the conversation.

Published by Stafford Weber of Team Stafford & Rebecca | Compass | Atlanta — your local guide to living in greater Atlanta.

What Most Sellers Get Wrong About Pricing Their Home

Many sellers believe listing their home as high as possible protects their equity. But that strategy can actually backfire. Here’s how a pricing strategy helps sellers attract buyers and maximize results in 2026.

Every year, right before the spring market kicks off, sellers say the same thing:

“We just don’t want to leave any money on the table.”

And they’re absolutely right. No one wants to sell their home only to wonder later if they could have gotten more.

So what do many sellers do?

They assume the way to protect themselves is to list as high as possible.

In theory, it makes sense. But that strategy can actually backfire.

Pricing matters even more now than it did during the peak years of 2022 and 2023. Buyers have more options, and they’re paying attention to everything: how long a home has been sitting on the market, whether the price has been reduced, and how it stacks up against the home down the street.

And that’s where many sellers run into trouble.

So today, let’s talk about the biggest mistakes sellers are making right now, and how to strategize list price instead.

Mistake #1: Treating List Price Like the Final Sales Price

Many sellers believe the list price is a statement.

Instead, think about it like an invitation.

The final sales price is determined later, after buyers:

View the home

Compare it to others

Compete (or don’t)

Submit offers

Negotiate

When you think of it as an invitation price, it’s easier to see that it simply controls how many people walk through the door in the first place.

Think of it like this:

If the invitation is too high, fewer buyers show up.

Fewer buyers means fewer offers.

Fewer offers means less leverage.

The goal isn’t to “pick the highest number.” The goal is to create positioning that attracts maximum demand.

Mistake #2: Believing Price Alone Determines the Outcome

Another major misconception: “If it doesn’t sell, it’s because the market is slow.”

Sometimes that’s true. But price is part of marketing. It’s one lever in a larger process that includes:

Presentation

Exposure

Timing

Buyer psychology

Negotiation strategy

Homes don’t sell solely because of a number. They sell because the strategy creates urgency and confidence.

When pricing is treated as a one-time guess instead of a strategic decision, sellers lose control of the outcome.

Mistake #3: Pricing Based on Old Comparables

A lot of sellers look at what their neighbor’s home sold for last year and assume that’s today’s value.

But markets shift.

The real story isn’t just what sold. It’s:

How many homes are currently active

How many are going under contract

How quickly they’re moving

When there are more homes for sale and fewer buyers, pricing aggressively can backfire.

When demand is strong and inventory is limited, pricing strategy looks different.

In short, your home doesn’t sell because of what happened 12 months ago. It sells based on what buyers are doing right now.

The 2026 Reality: Buyers Are More Analytical

Today’s buyers:

Compare multiple properties instantly.

Track price reductions.

Watch days on market.

Study past sales history.

If a home sits without activity, buyers assume something is wrong, even when it isn’t.

That’s what a home that starts too high often ends up selling for less than it would have if it had been positioned correctly from day one.

Momentum matters.

So, How Should Sellers Think About Pricing?

Instead of asking: “How high can I list?”

Ask: “What pricing strategy will create the strongest position in today’s market?”

There are generally three approaches:

Aspirational Pricing: Starting high and testing the market. This can work for rare or highly unique homes, but often requires adjustments.

Market-Positioned Pricing: Pricing in line with current competition to attract steady, predictable activity.

Event-Based Pricing: Pricing to generate maximum attention early and create competitive momentum.

The right strategy depends on:

Your timeline

Your goals

Current local inventory

Buyer demand in your price range

Final Thought

The best deal for a seller is one that meets their goals while protecting their equity. That includes the price, of course, but also the terms of the offer, the likelihood of a smooth inspection, a clean appraisal, and the chances of the deal closing without constant renegotiation.

Sometimes that surprises sellers, especially when the highest offer isn’t the strongest one.

For example, if a homeowner needs to move quickly, a slightly lower cash offer with a fast closing can be far more appealing than a higher financed offer that comes with a longer timeline and more uncertainty.

In other words, success isn’t just about chasing the biggest number. It’s about choosing the strategy that gets you the best result. And that’s especially true in today’s market.

In 2026, the market isn’t punishing sellers. It’s rewarding strategic ones.

So if you’re thinking about selling this year, the real question shouldn’t be:

“How high can we price it?”

Instead, it should be:

“How do we position the home to win?”

That shift alone can completely change the outcome of your sale.

-Stafford Weber | Stafford & Rebecca | Compass Atlanta

Homebuyers Just Gained $30K in Purchasing Power

Buying power is up $30K, and rates dipped to 5.99%, giving homebuyers in Atlanta more options this spring.

Stafford & Rebecca | Compass Atlanta

A year ago, a lot of homebuyers in Atlanta, ran the numbers and didn’t like what they saw.

Today, those numbers look different.

According to Zillow, a median-income household can now afford $30,302 more home than they could a year ago.

The reason? Mortgage rates have eased from nearly 7% last winter to around 6%, and recently dipped to 5.99%.

That alone lowers the monthly payment enough to change what many buyers qualify for.

Here in Atlanta, the real question isn’t what’s happening nationally. It’s what this means for you, your budget, and the neighborhoods you’ve been watching.

Let’s walk through what’s changed and how it affects your next move.

You May Qualify for More Than You Think

If you looked at homes in Atlanta, last year and felt boxed in by your budget, it may be worth revisiting those numbers.

Mortgage rates averaged 6.96% in early 2025. And this week, they dipped to 5.99%. That lowers the monthly payment enough to increase what many buyers can qualify for.

Here’s the math for a $3,000 monthly budget:

With a 5.99% mortgage rate, buyers can now afford roughly a $479,750 home.

At the start of this year, when rates were around 6.2%, that same budget bought about $471,750.

A year ago at 6.9%, it bought $446,000.

That’s an $8,000 gain in just the past few weeks and $33,750 more purchasing power than a year ago.

(Note: The above example assumes 20% down, a 30-year mortgage,1.25% property tax rate, 0.5% homeowners' insurance rate, and no HOA dues.)

Of course, the only way to know what it means for your budget is to rerun the math based on today’s rates, today’s prices in Atlanta, and your current income.

What This Means for Your Plan in Atlanta

If you pressed pause on buying over the past year, this is a good time to look at your options again.

Buyers now need about $111,000 in income to afford the typical U.S. home, down 4% from last year. Affordability is improving in 37 of the 50 largest metros.

If rates stay near 6% (or better yet, under), affordability will continue to improve.

Here’s what that could mean in Atlanta

Checking what you qualify for at today’s rates

Expanding your search into neighborhoods that were slightly out of reach

Paying attention to homes that have been sitting and may have room for negotiation

For homeowners, it could also mean scoring a lower monthly payment with a refi.

The point is, you don’t have to rush. Or stretch your budget to the breaking point. In fact, don’t do that. Being house-poor is not the goal. But you do want clear numbers and a simple plan.

Right now, the numbers are lining up in a way they haven’t in a while. Lower rates + Slower price growth.

If you’re wondering what you can afford right now in Atlanta, the smartest first step is running the numbers based on today’s rates, today’s prices, and your actual budget.

Once you have that clarity, your next move gets much easier to decide.

-Stafford Weber | Compass

Team Stafford & Rebecca | Compass Atlanta

7 Housing Market Data Points That Push Back on the Doomer Narrative

Housing affordability in 2026 looks different from what doomer Tweets suggest, with lower payments, more seller inventory, and improving rent trends.

Housing is expensive. Rates are higher than they were in early 2020. Home prices have gone up. Rent hasn’t exactly been a bargain either.

So, when a bold graphic like this one shows up in your feed confirming that frustration, it’s easy to assume that’s the whole story.

The good news? It’s not.

Because affordability isn’t just about home prices. It’s about mortgage rates, wage growth, housing inventory, negotiating power, and even local supply. And over the past several months, some of those pieces have started moving in a better direction.

So, before you make a major decision based on a social media post, let’s look at what the data actually says and how it applies to real people in real markets, including ours.

1. Mortgage Rates Have Eased and Refinancing Is Back on the Table

Let’s start with mortgage rates, because they drive the monthly payment more than almost anything else.

As of mid-February, the average 30-year fixed rate is sitting around 6.05%. Still a far cry from the 3% rates we were seeing in early ‘22, but it’s meaningfully lower than where we were when rates were pushing 7% and higher.

In early January, rate declines opened up refinance opportunities for nearly five million borrowers nationwide. Five million households suddenly had a chance to lower their monthly payment by a significant amount.

For some families, that’s enough breathing room to avoid foreclosure. For others, it’s the difference between feeling stretched and feeling stable (and even saving for something fun).

Affordability recently hit its highest level in four years, according to national data. That doesn’t mean homes are “cheap,” but it does mean the pressure is easing compared to where we were.

Now here’s where this gets personal.

If you already own a home, a small rate drop could mean it’s worth running the numbers on a refinance. If you’re thinking about buying, the difference between 6.8% and 6.0% can change your monthly payment more than a modest shift in price ever would.

In our local market, rates and inventory are interacting in their own way. The only way to know what that means for you is to look at the local numbers, not a viral chart.

2. The Buy vs Rent Gap Is Smaller Than It’s Been in 3 Years

For a while, buying felt so far out of reach that a lot of renters stopped even running the numbers.

Nationally, buyers need about $111,000 in annual income to afford a typical home. Renters need about $76,000 to afford a typical apartment.

That gap is $35,000. It’s still real money, but it’s the smallest it’s been in three years.

A couple years ago, the gap was wider and moving in the wrong direction. Today, it’s narrowing. Mortgage rates have dropped. Home price growth has slowed. And wages have continued to rise. It doesn’t suddenly make buying easy, but it does mean the math isn’t as brutal as it was a couple years ago.

If you’re renting right now, this is where things get practical.

The question isn’t “Is housing expensive?” It is. Obviously. The better question is whether the difference between renting and owning still makes sense for you long term. In some cases, the monthly payment gap isn’t as dramatic as it was in 2022. In others, it still is.

If you’re trying to decide whether to renew your lease or explore buying, the smartest move is to compare real numbers side by side.

Not internet opinions. Not headlines. Just the math tied to your income and your goals.

3. Monthly Payments Actually Came Down in 2025

When people talk about affordability, what they’re really asking is, “What would my monthly payment be?”

In 2025, homebuyer affordability improved 7.5% nationwide. The median mortgage payment dropped to $2,025. That’s $102 less per month than the year before.

Lower mortgage rates played a big role, and household incomes continued to grow.

Over twelve months, that $102 adds up to more than $1,200. For some families, that covers a car repair. For others, it helps build savings. It’s not dramatic, but it makes a difference.

The payment is also taking up a slightly smaller portion of the typical household’s income than it did at the start of the year. That tells us the squeeze isn’t as tight as it was.

Here in Atlanta, the actual payment depends on the price range, property taxes, insurance, and whether there are HOA fees. National averages are helpful, but your real number is what matters.

4. Renters Are Getting Some Relief, Too

If you’re renting right now, you’ve probably felt the pressure the past few years.

Renewals kept coming in higher. Available units filled fast. Negotiating wasn’t really a thing.

That pace has cooled. A bit.

Nationally, the typical household is spending 26.4% of its income on rent. That’s the lowest share since August 2021. The typical asking rent in January was $1,895. That’s flat month over month and up just 2% from a year ago, making it the slowest annual growth since 2020.

More units have come online. Vacancy rates are higher. Nearly 40% of rental listings are even offering concessions like free months or reduced deposits. That means renters today have more leverage than they did when landlords could raise prices and fill a unit within days.

Here in Atlanta, conditions vary by neighborhood and property type. Some areas are still tight. Others are offering flexibility that just wasn’t available a couple of years ago.

If your lease is up soon, it’s worth having a conversation before you automatically accept the renewal terms.

5. Builders Are Cutting Prices

A lot of people assume new construction is the expensive option. Right now, that’s not always true.

In the fourth quarter of 2025, 19.3% of new homes had price cuts. That’s slightly higher than the 18.3% of existing home sellers who reduced their price during the same period. In other words, builders are negotiating.

Some of that activity is concentrated in the South and West. Builders in those regions ramped up production, and now they’re adjusting to keep homes moving. That can show up as straight price reductions, mortgage rate buydowns, or closing cost incentives.

If you’ve only been looking at resale homes, it might be time to widen the search. A builder offering a rate buydown can change your monthly payment in a way a small price reduction on an existing home might not.

Here in our market, some builders are offering incentives on the down-low. They won’t always advertise the best terms on the sign out front. You often have to ask.

New construction isn’t automatically a bargain. But it’s not automatically out of reach either.

6. In Many Markets, Buyers Finally Have More Room to Breathe

For the first time in a while, buyers aren’t competing with ten other offers on every house.

Nationally, there are 37% more sellers than buyers. That’s more than double the gap from last year. In some cities, the difference is even wider. Austin has 114.3% more sellers than buyers. Charlotte sits at 78.1%, still well above the national average.

There are still pockets of the country where sellers hold the upper hand. Nassau County, New York, for example, has 39.1% fewer sellers than buyers. But overall, the balance has tilted in favor of buyers in many areas.

What does that actually mean for you?

It means homes are sitting a little longer. It means price reductions are more common. It means you may be able to negotiate repairs, credits, or a better purchase price without feeling rushed.

If you stepped back from the market in 2021 or 2022 because it felt chaotic, today looks different. You have more time to think. You can compare options. You can walk away from a deal that doesn’t make sense or just doesn’t feel right.

Here locally, inventory levels and days on market tell the real story. Some neighborhoods are still competitive. Others are clearly leaning toward buyers.

The key is knowing which is which before you make a move.

7. No One Serious Is Predicting a Crash

A lot of people are still waiting for “the crash.”

You see it in the comments. “Just wait.” “It’s all coming down.” “This is 2008 all over again.”

Here’s the problem with that narrative. The people who actually study this stuff for a living aren’t predicting that.

Home price forecasts for 2026 range from a slight dip of -0.3% to modest growth of +4.3%. That’s not a boom. It’s not a collapse either. It’s a pretty tight range.

Every major forecast expects home sales to increase from the 4.06 million total in 2025. Projections call for growth somewhere between 1.7% and 14%. That’s an expansion, not a freeze.

Mortgage rate forecasts land between 6.0% and 6.5% for the year’s average. January closed at 6.16%, down from 6.85% a year earlier. That’s gradual improvement, not chaos.

Could something unexpected happen? Of course. Markets are influenced by the economy, jobs, inflation, and policy.

But based on the data in front of us, no major economist is calling for a housing crash.

If you’ve been holding off because you’re convinced prices are about to fall off a cliff, it’s worth looking at what would actually need to break for that to happen. Right now, the numbers point to a market that’s working through affordability challenges, not one on the edge of implosion.

The Full Picture Is Bigger Than a Viral Chart

If you only look at one graph, it’s easy to feel discouraged.

Yes, prices went up. Rates jumped. Rents climbed. That part is real.

What usually gets left out is what’s happened since. Rates have eased from their highs. Monthly payments came down last year. Rent growth has slowed. Builders are offering price cuts and incentives. In many markets, buyers finally have time to think instead of scrambling to win a bidding war. And the people who analyze housing for a living are not forecasting a crash.

Affordability is still tight. Homes are still expensive. And yet, the recent data shows gradual improvement over the past year.

If you’re trying to decide whether to buy, sell, refinance, or renew your lease, the only numbers that really matter are yours. Your income. Your timeline. Your plans here in Atlanta.

That’s a more productive conversation than any viral chart.

-Stafford and Rebecca | Compass Atlanta

Selling in Atlanta? Zillow Data Shows What Buyers Care About Now

Zillow analyzed 20 years of listings and found buyers value livability, lower costs, and practical layouts more than size or formality.

-Stafford & Rebecca | Compass

If you’re thinking of selling in 2026, you might think bigger rooms, formal spaces, and neutral paint colors equal higher value.

But today’s buyers aren’t shopping that way anymore, and new Zillow data backs that up.

After reviewing 20 years of for-sale listings, Zillow found buyers now care more about practical layouts and manageable sizes, along with features that help keep long-term costs under control.

To understand why, it helps to look at how home design priorities have changed over the past two decades, starting with the rise and fall of the McMansion era.

Why Bigger Doesn’t Automatically Mean More Valuable Anymore

For a long time, size felt like a safe bet. More square footage was easy to point to when justifying price, especially during the height of McMansion-style homes.

Zillow’s 20-year review shows newer homes have been getting smaller, not larger, and buyer interest has followed.

Cost and usability are driving that change. Bigger homes often bring:

Higher energy bills

Higher insurance premiums

More ongoing maintenance

Oversized rooms and dramatic features like two-story foyers still photograph well, but they get buyers thinking:

How expensive will this be to heat and cool?

Will this space feel drafty or uneven in temperature?

How expensive is it to insure a house with this much volume?

How much of this space will we actually use?

What does it cost to replace or repair windows this size?

Many buyers now see more value in how well a home functions and how manageable it feels to live in. A smart layout with a reasonable footprint often connects more than extra square footage that drives up monthly costs.

Layouts, Finishes, and What Actually Stands Out to Buyers

Once buyers are inside the home, Zillow’s listing data shows they’re placing less value on rooms designed for occasional use and more on spaces that serve a clear purpose.

That shift shows up in how buyers evaluate layouts:

Openness where it helps everyday living

Separation where privacy or quiet matters

Spaces that feel usable year-round

Zillow has seen a 48% increase in listings mentioning reading nooks, pointing to demand for contained, quiet spaces within the home.

Buyers are asking themselves whether there’s a place to work, take a call, or decompress, and whether the layout works when the house is full, not just when it’s staged.

Design choices are being judged differently, too.

Many sellers still default to neutral finishes to avoid turning buyers off. Zillow’s data suggests that approach doesn’t always pay off. Mentions of color drenching are up 149%, and Zillow’s paint analysis found buyers were willing to offer more for homes painted in darker colors like:

Olive green

Navy blue

Charcoal gray

The goal isn’t to chase paint color trends, but to avoid stripping away personality in the name of playing it safe.

What Buyers Mean Now When They Talk About “Good Upgrades”

Upgrades used to mean finishes. But today’s buyers are focused on features that affect comfort, monthly costs, and long-term reliability.

Zillow’s data shows growing interest in wellness and efficiency features:

Spa-inspired bathrooms are up 22%

Golf simulators are up 25%

Pickleball courts are up 25%

Energy-related features are gaining even more traction:

Zero-energy-ready homes are up 70%

Whole-home batteries are up 40%

EV charging stations are up 25%

During showings, these upgrades prompt planning-focused questions:

What will our utility bills look like?

How insulated and efficient is this home?

Is it set up for electric vehicles or future energy needs?

Will these features help protect us from rising insurance or climate risks?

Zillow notes that climate-resilient features are increasingly being called out as selling points. Features that lower ongoing expenses and reduce uncertainty often carry more weight than finishes that look new but cost more to maintain.

When buyers leave a showing, they’re deciding whether the home feels workable for real life, not just appealing on paper. Homes that communicate efficiency and livability tend to connect more strongly in today’s market.

I’ll leave you with this perspective from Zillow home trends expert Amanda Pendleton:

“If the past 20 years transformed homes from status symbols into personal sanctuaries, the next 20 will be about adaptability. Our homes will be better able to evolve with changing families, changing climates and changing lifestyles.

We expect future homes to be more flexible, resilient and deeply personal. The smartest homes won't feel high-tech; they'll feel intuitive, lived-in and supportive.”

Top ROI Projects to Boost Your Home’s Value Before Selling in 2026

Simple home improvements with proven ROI can boost your sale price in Atlanta. See where to invest your prep dollars for the biggest returns. - Stafford & Rebecca, Compass.

When you prepare to sell your Atlanta home, every dollar you spend before listing should have one job: come back to you in the form of a higher sale price.

The challenge for most homeowners isn’t deciding whether to update their home. It’s figuring out where those prep dollars will work hardest. Some projects bring back two or even three times what they cost, while others barely move the needle.

The good news? You don’t need a full renovation to maximize your profit. A handful of targeted, high-ROI improvementscan dramatically improve how buyers perceive your home and how strong their offers are.

Here’s what to focus on if you want the biggest return with the least stress.

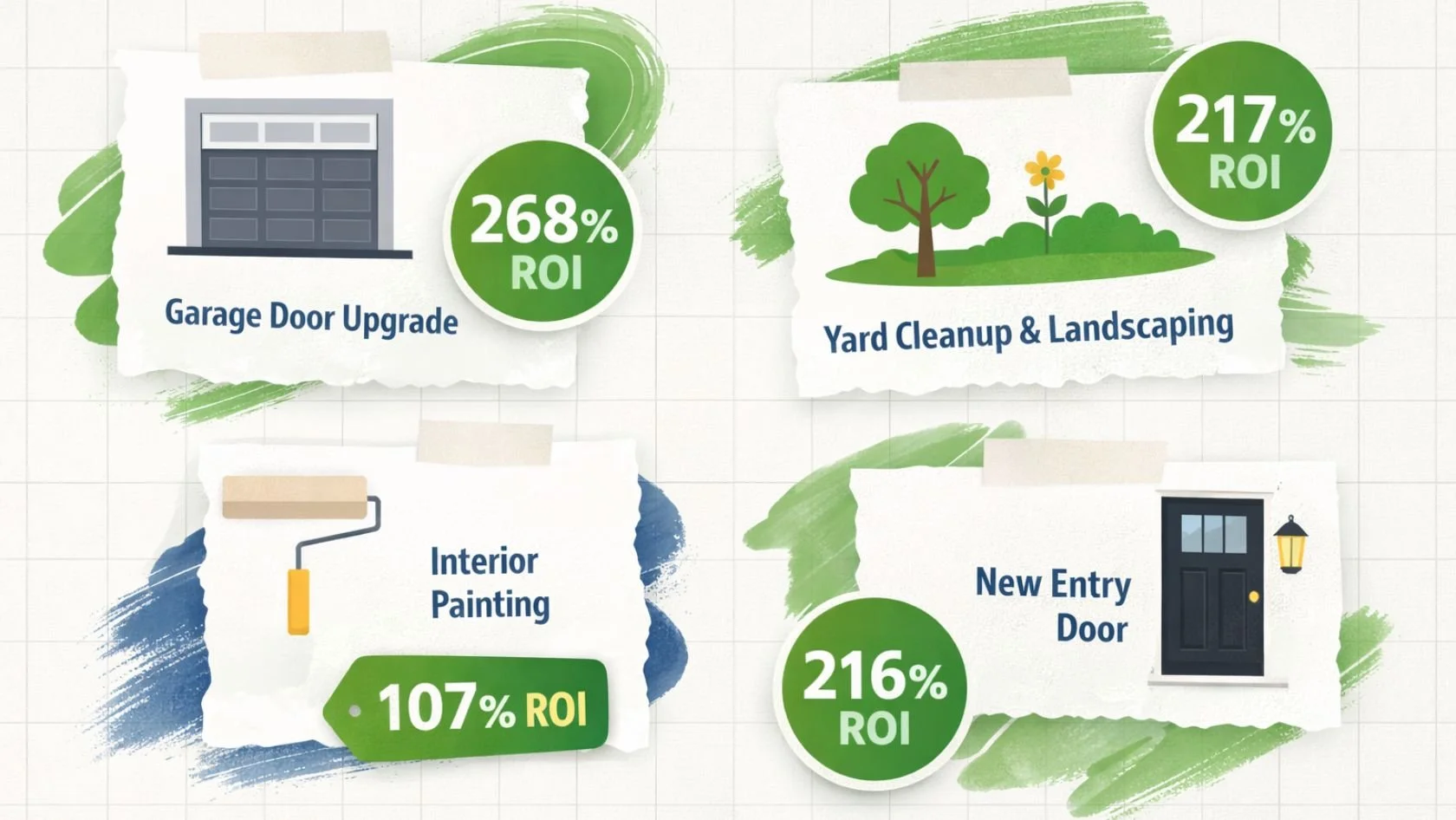

The Highest-Return Projects That Boost Value Fast

First impressions matter more than most sellers realize. Curb appeal and visible upgrades often shape how buyers feel about a home before they even walk inside.

Some of the strongest ROI projects nationwide include:

Garage door refresh or replacement

Average cost: about $4,672

Resale value added: roughly $12,507

ROI: 268%

Basic lawn care and yard cleanup

Average cost: around $415

Resale value added: about $900

ROI: 217%

Steel entry door replacement or upgrade

Average cost: roughly $2,435

Resale value added: about $5,270

ROI: 216%

Manufactured stone veneer accents

Average cost: around $11,702

Resale value added: roughly $24,328

ROI: 208%

Buyers often decide within minutes whether a home feels well cared for. These projects send a clear signal that the property has been maintained and is move-in ready.

Low-Cost DIY Updates That Still Deliver Big Returns

You don’t need a massive budget to make a noticeable difference. Some of the most affordable improvements consistently bring back more than they cost.

Here are a few seller favorites:

Interior painting in neutral tones

Cost: about $2 to $6 per square foot

Resale value added: roughly $1,070 to $3,210

ROI: 107%

Hardwood floor refinishing

Average cost: around $3,400

Resale value added: about $5,000

ROI: 147%

Closet shelving and organization upgrades

Cost: about $500 to $2,500

Resale value added: roughly $2,000

ROI: 55% to 60%

Basic landscaping refresh

Cost: about $4,800 to $9,000

Resale value added: roughly $5,000 to $9,000

ROI: 100% to 104%

These projects improve how your home looks in photos, during showings, and in online listings, which is especially important in today’s digital-first home search.

Mid-Range Improvements That Still Pay Off

For homeowners with a little more time or budget before listing, these upgrades tend to deliver solid value while making homes more attractive to buyers.

Some strong performers include:

New wood deck

Average cost: about $18,263

Resale value added: roughly $17,323

ROI: 95%

Concrete paver patio

Average cost: around $10,500

Resale value added: about $10,000

ROI: 95%

Fiber-cement siding replacement

Average cost: roughly $21,485

Resale value added: about $24,420

ROI: 114%

Smart-home upgrades

Average cost: around $3,026

Resale value added: roughly $2,633

ROI: 87%

Outdoor living spaces and efficiency-focused features continue to attract buyers, especially as people think more about comfort and long-term costs.

How to Prioritize Home Prep in Atlanta

Every home and budget is different, but a smart strategy usually follows a few simple principles.

Before spending on upgrades, homeowners should:

Start with projects buyers notice in the first few minutes of a showing

Focus on improvements with 100%+ ROI whenever possible

Match upgrades to the price range and expectations in [Your Market]

Avoid over-customized renovations that don’t translate to higher offers

Finally, be sure to consult with your real estate agent. Many times, sellers think their home needs multiple upgrades when in reality, it just needs some deep cleaning or staging.

The goal, here, is to focus on the updates that actually move your home’s value in the right direction. Strategic, ROI-backed improvements consistently lead to stronger offers and faster sales, not to mention less stress during negotiations.

Wondering what your home is worth? Reach out!

Stafford & Rebecca | Compass

Fulton County Senior Property Tax Relief Begins in 2026 — What Homeowners Should Know

Beginning in 2026, many senior homeowners in Fulton County will see meaningful relief on the school tax portion of their property taxes.

By Stafford Weber | Atlanta Real Estate

Beginning in 2026, many senior homeowners in Fulton County will see meaningful relief on the school tax portion of their property taxes. These new exemptions, approved by voters, are designed to help long-time residents remain in their homes as property values and tax bills continue to rise across the Atlanta area.

Here is what homeowners need to know.

What Is Changing in 2026

Starting January 1, 2026, eligible seniors will receive a reduction in the school tax portion of their property taxes:

Age 65–69 → 25% reduction

Age 70+ → 50% reduction

No income limitation

This exemption applies to qualified homeowners within Fulton County and, depending on location, may interact differently with either Fulton County Schools or Atlanta Public Schools tax structures.

Who Qualifies

To receive the exemption, homeowners must meet the following criteria:

Be 65 years or older (based on age as of January 1, 2026)

Maintain a homestead exemption on the property

Use the home as their primary residence

Have held homestead status for at least 5 of the past 6 years

These requirements are intended to benefit long-term homeowners rather than short-term property holders.

Is the Exemption Automatic?

Some eligible homeowners may see this exemption applied automatically. However, not every situation is identical, and homeowners should not assume it has been applied without verification.

The safest step is to confirm eligibility directly with the Fulton County Tax Assessor’s Office, especially if:

You recently turned 65

You moved within Fulton County

Your homestead status changed in recent years

Deadlines for homestead-related filings are typically April 1 each year, so early verification is wise.

What This Means Financially

For many seniors, this exemption could reduce annual property taxes by hundreds to several thousand dollars, depending on home value and school tax exposure.

More importantly, this relief helps:

Improve long-term housing affordability

Allow seniors to remain in their homes longer

Reduce financial pressure as property values rise

A Broader Trend in Atlanta

Across Atlanta, we are seeing increased focus on helping long-time homeowners maintain stability in neighborhoods experiencing growth and rising values. Programs like this reflect the reality that property taxes — not just housing prices — play a major role in long-term homeownership decisions.

For some homeowners, this new exemption may influence:

Decisions about staying vs. downsizing

Long-term financial planning

Estate and legacy planning

Timing of a potential move

Final Thoughts

This new 2026 senior tax relief represents meaningful support for many Fulton County homeowners — but eligibility and application details matter. Verifying your status early ensures you receive the full benefit available to you.

If you or a family member would like help:

Understanding eligibility

Estimating potential tax savings

Evaluating how this impacts long-term housing decisions

I’m always happy to be a resource.

5 Things Homebuyers Don’t Actually Care About (and What Really Matters)

Discover what home buyers really care about, and what they don’t. Learn the common mistakes sellers make, so you can focus on what makes the biggest impact on the sale of your home.

Most sellers start with good intentions. You want the house to look great. So you Google what to fix before selling, skim a few articles, and suddenly it feels like your entire home needs an upgrade.

The list grows fast. New paint. New floors. New counters. New fixtures.

Before long, selling feels like a renovation project. But here’s the truth most sellers don’t hear until it’s too late:

Buyers care far less about many of those details than you think.

And focusing on the wrong things can cost you time, money, and momentum in today’s market.

Let’s break down what buyers don’t care about (and what they really pay attention to instead).

5 Things Buyers Rarely Care About (As Much as Sellers Think)

1) Your personal style

You might love your bold accent walls, custom wallpaper, or unique design choices.

Buyers walk in ready to imagine their own furniture, colors, and layout.

Most buyers don’t fall in love with décor. They fall in love with space, light, and layout.

What matters more:

Open, functional floor plans

Natural light

Room size and flow

2) Small cosmetic upgrades

Many sellers assume that every upgrade adds dollar-for-dollar value.

In reality, buyers often see things like:

New cabinet hardware

Mid-range appliances

Trendy backsplashes

Minor landscaping

as “nice to have,” not “pay more for.”

What matters more:

Overall condition compared to similar homes

Major updates (roof, HVAC, windows, kitchens, bathrooms)

3) Highly customized features

That custom wine room, built-in aquarium, or themed home office might feel luxurious to you.

To buyers, it can feel limiting.Highly personalized features often make buyers think:

“How much will it cost to undo this?”

What matters more:

Neutral, flexible spaces

Rooms that can serve multiple purposes

4) Minor imperfections

Sellers often panic over tiny flaws:

Small wall cracks

Slightly worn floors

Outdated light fixtures

Minor scuffs or scratches

Most buyers expect some wear and tear.

What matters more:

Structural integrity

Roof condition

Plumbing, electrical, and HVAC

Signs of water damage

5) How much money you spent on the home

It’s natural to think:

“I invested so much into this house. It has to be worth more.”

But buyers don’t purchase homes based on your investment. They price them based on the market.

What matters more:

Comparable home sales

Location

Supply and demand

So what do buyers actually care about?

When it comes down to it, buyers are asking one simple question:

“Is this home worth the price compared to my other options?”

They care about:

Location

Layout and space

Condition of major systems

Price relative to the market

Long-term value

And what makes buyers walk away?

Now for the short list that really matters. These are the issues that make buyers nervous and sometimes send them straight to the next showing.

Roof problems or obvious signs of major wear

Water damage, leaks, or ongoing moisture issues (often tied to mold)

Foundation cracks or floors that feel uneven

Big electrical or plumbing problems

HVAC systems that aren’t working properly or look near the end of their life

Fire damage or strong lingering smoke smells

Cosmetic stuff leads to negotiation. Big problems lead to second thoughts.

The takeaway for sellers

Homes don’t need to be perfect to sell well. They do need to feel solid, clean, and well cared for.

Most buyers are happy to update paint colors and finishes over time. What they don’t want are surprise repairs and big unknowns.

If you’re thinking about selling this spring, the smartest move is usually getting on the market sooner with a well-prepared home, not waiting months chasing upgrades that won’t change the outcome.

The Buyer-Seller Balance Has Flipped. Here’s What That Means for You

If you’re looking to buy a home in 2026, and you’ve been waiting for the housing market to feel a little less stacked against you, that moment may finally be here.

According to a recent Redfin report, buyers now have more negotiating power than they’ve had in over a decade. In fact, sellers now outnumber buyers by a record margin.

That doesn’t mean the market is suddenly easy for home shoppers, but it does mean you’re no longer expected to rush into decisions just to keep up.

Understanding what’s changing can help you approach your home search with more clarity.

Why Buyers Have More Leverage Right Now

The biggest reason you’re gaining leverage is simple. Across the nation, there are 47.1% more sellers than buyers in today’s housing market. When that happens, sellers have to work harder to stand out. And you gain more options to choose from.